4. The Discount Factor

4. The Discount Factor

本章导读 本章(Cochrane 第 4 章)问一个更基本的问题:贴现因子 \(m\) 从哪来? 答案出人意料地廉价。仅凭价格与支付的两条性质,就能反推出 \(m\) 的存在与正性,完全不必假设效用、完全市场或均衡。§4.1 一价定律 (law of one price) \(\Rightarrow\) 存在一个支付空间内的贴现因子 \(x^*\),并给出显式构造 \(x^*=p'\mathbb E(xx')^{-1}x\);§4.2 无套利 (no-arbitrage) \(\Rightarrow\) 存在严格为正的贴现因子 \(m>0\)(由分离超平面定理给出,但不唯一);§4.3 \(x^*\) 的另一种(均值-协方差)表达式,及其连续时间形式。

4. The Discount Factor

Overview This chapter (Cochrane Ch 4) asks a more basic question: where does the discount factor \(m\) come from? The answer is surprisingly cheap. From just two properties of prices and payoffs we can back out the existence and positivity of \(m\) — with no assumption of utility, complete markets, or equilibrium. §4.1 the law of one price \(\Rightarrow\) there exists a discount factor \(x^*\) inside the payoff space, with the explicit construction \(x^*=p'\mathbb E(xx')^{-1}x\); §4.2 no-arbitrage \(\Rightarrow\) there exists a strictly positive discount factor \(m>0\) (delivered by the separating hyperplane theorem, but not unique); §4.3 an alternative (mean-covariance) expression for \(x^*\) and its continuous-time form.

4.1 一价定律与贴现因子的存在 / Law of One Price and the Existence of a Discount Factor

我们一直把 \(p=\mathbb E(mx)\) 当作出发点。本节反过来:把价格与支付当作原始对象,问什么条件下能找到一个 \(m\) 使 \(p=\mathbb E(mx)\) 成立。设支付空间为 \(X\)(可交易的支付集合),定价函数 \(p(x)\) 把每个支付映到今天的价格。我们只要求 \(p(\cdot)\) 满足两条性质:

4.1 Law of One Price and the Existence of a Discount Factor

We have been treating \(p=\mathbb E(mx)\) as a starting point. This section turns it around: take prices and payoffs as the primitive objects, and ask under what conditions we can find an \(m\) such that \(p=\mathbb E(mx)\) holds. Let \(X\) be the payoff space (the set of tradeable payoffs), and let the pricing function \(p(x)\) map each payoff to its price today. We require only two properties of \(p(\cdot)\):

- A1(组合构造 / portfolio formation):\(x_1,x_2\in X\Rightarrow ax_1+bx_2\in X\)(支付空间对线性组合封闭)。

- A2(一价定律 / law of one price):定价是线性的,

- A1 (portfolio formation): \(x_1,x_2\in X\Rightarrow ax_1+bx_2\in X\) (the payoff space is closed under linear combinations).

- A2 (law of one price): pricing is linear,

$$p(ax_1+bx_2)=a\,p(x_1)+b\,p(x_2).$$

A2 即"一价定律":同一支付无论由哪些证券组合而成,价格都相同——否则可低买高卖。注意 A1、A2 都很弱:不需要完全市场(\(X\) 可以是 \(\mathbb R^S\) 的真子空间),不需要无套利,更不需要效用或均衡。仅此两条就足以得到一个贴现因子:

A2 is the "law of one price": the same payoff has the same price no matter which securities are combined to form it — otherwise one could buy low and sell high. Note A1 and A2 are both weak: no complete markets (X may be a proper subspace of \(\mathbb R^S\)), no no-arbitrage, and certainly no utility or equilibrium. These two alone suffice to deliver a discount factor:

贴现因子存在定理 / Existence theorem 在 A1、A2 下,存在唯一一个支付 \(x^*\in X\),使得对每个 \(x\in X\) 都有 \(p(x)=\mathbb E(x^*x)\)。这个 \(x^*\) 就是一个(在支付空间内的)贴现因子。Given A1 and A2, there exists a unique payoff \(x^*\in X\) such that \(p(x)=\mathbb E(x^*x)\) for every \(x\in X\). This \(x^*\) is a discount factor (one that lives inside the payoff space).

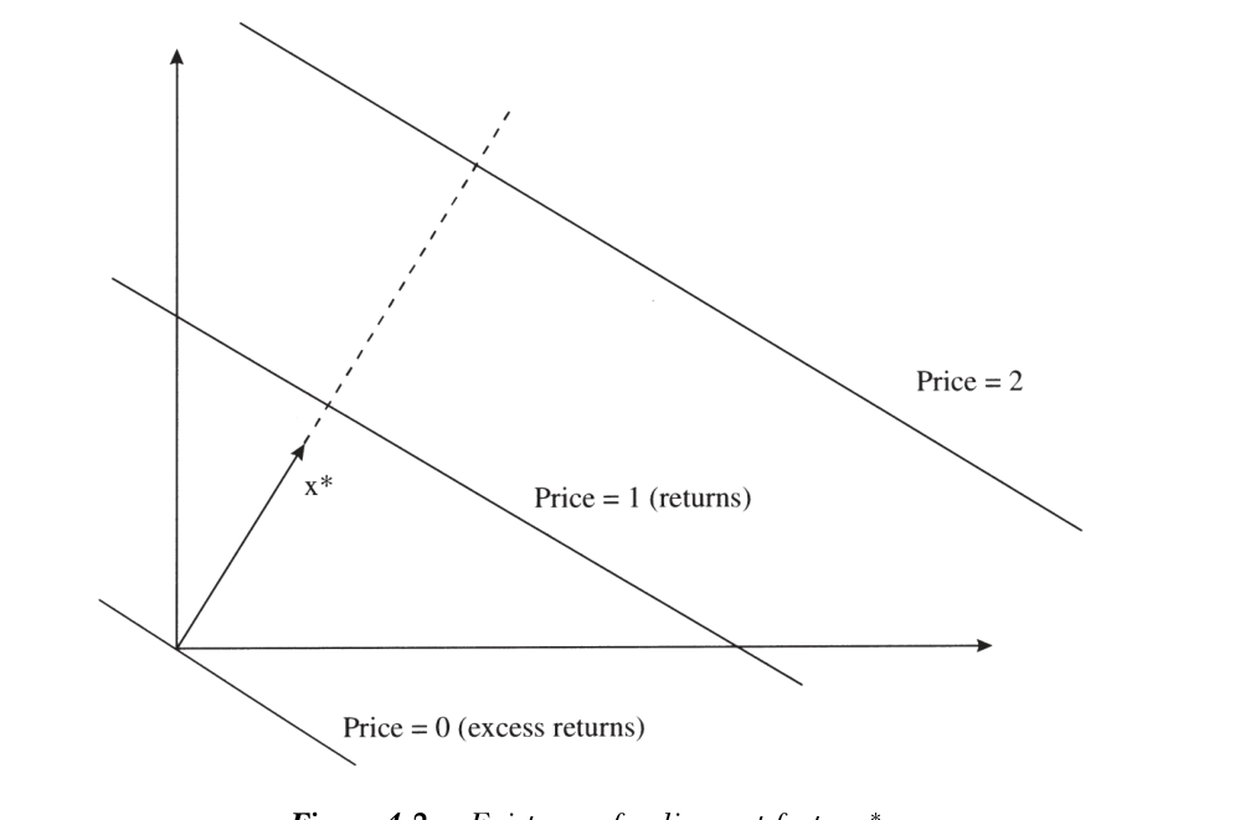

证明一(几何 / 构造)。 关键的数学事实是:任何线性函数都可表示为内积。在支付空间 \(X\) 上以 \(\mathbb E(xy)\) 为内积,定价 \(p(\cdot)\) 是 \(X\) 上的线性函数,故存在某个 \(x^*\in X\) 使 \(p(x)=\mathbb E(x^*x)\)。几何上:价格为 1 的支付构成一张超平面("\(\text{Price}=1\)"),价格为 0 的支付(超额收益)构成过原点、与之平行的超平面。沿这些平面的法线方向取一个向量,调到合适长度,使其在 \(\text{Price}=1\) 平面上的支付的内积恰为 1,这个向量就是 \(x^*\)。无穷维情形由 Riesz 表示定理 保证(Hansen and Richard 1987)。

Proof 1 (geometric / constructive). The key mathematical fact is that any linear function can be represented as an inner product. Equip the payoff space \(X\) with the inner product \(\mathbb E(xy)\); pricing \(p(\cdot)\) is a linear function on \(X\), so there is some \(x^*\in X\) with \(p(x)=\mathbb E(x^*x)\). Geometrically: the payoffs with price 1 form a hyperplane ("\(\text{Price}=1\)"), and the price-0 payoffs (excess returns) form a parallel hyperplane through the origin. Take a vector along the normal to these planes and scale it so that its inner product with any price-1 payoff equals 1 — that vector is \(x^*\). The infinite-dimensional case is guaranteed by the Riesz representation theorem (Hansen and Richard 1987).

下图画出了这一几何:\(\text{Price}=0\)、\(\text{Price}=1\)、\(\text{Price}=2\) 是一族平行的等价格线,\(x^*\) 沿它们的公共法线方向,长度恰好使其落在 \(\text{Price}=1\) 线上。

图 4.2 贴现因子 \(x^*\) 的存在性。等价格线相互平行,\(x^*\) 沿其公共法线,长度使其位于 \(\text{Price}=1\) 线上。

Figure 4.2 Existence of a discount factor \(x^*\). The constant-price lines are parallel; \(x^*\) lies along their common normal, scaled to sit on the \(\text{Price}=1\) line.

证明二(代数 / 构造)。 当支付空间由 \(N\) 个基础支付张成时(例如 \(N\) 只股票),可显式构造。把基础支付排成向量 \(x=[x_1\;x_2\;\cdots\;x_N]'\),对应价格 \(p\),支付空间 \(X=\{c'x\}\)。我们要找形如 \(x^*=c'x\) 的贴现因子,使它给基础资产定出正确价格:\(p=\mathbb E(x^*x)=\mathbb E(xx'c)=\mathbb E(xx')c\)。于是 \(c=\mathbb E(xx')^{-1}p\)(A2 保证 \(\mathbb E(xx')\) 非奇异),代回得显式公式:

Proof 2 (algebraic / constructive). When the payoff space is generated by \(N\) basis payoffs (e.g. \(N\) stocks), we can construct \(x^*\) explicitly. Stack the basis payoffs into a vector \(x=[x_1\;x_2\;\cdots\;x_N]'\) with prices \(p\), so \(X=\{c'x\}\). We seek a discount factor of the form \(x^*=c'x\) that prices the basis assets correctly: \(p=\mathbb E(x^*x)=\mathbb E(xx'c)=\mathbb E(xx')c\). Hence \(c=\mathbb E(xx')^{-1}p\) (A2 guarantees \(\mathbb E(xx')\) is nonsingular), and substituting back gives the explicit formula:

$$x^*=p'\,\mathbb E(xx')^{-1}\,x.\tag{4.1}$$

这个公式在实证中非常有用:给定一组资产的价格 \(p\) 与支付的二阶矩 \(\mathbb E(xx')\),(4.1) 直接给出落在这些资产张成空间内的贴现因子。

任何能给 \(X\) 中支付定价的贴现因子 \(m\),都可写成 \(m=x^*+\varepsilon\),其中 \(\mathbb E(\varepsilon x)=0\)(即 \(\varepsilon\) 与所有支付正交)。换言之,\(x^*\) 是 \(m\) 在支付空间上的正交投影 \(x^*=\operatorname{proj}(m\mid X)\),是贴现因子的"模仿组合 (mimicking portfolio)":定价只用得上 \(m\) 落在支付空间里的那一部分,正交部分 \(\varepsilon\) 对所有可交易支付的定价毫无贡献。这呼应了第 1 章"特异性风险不被定价"的道理。

This formula is very useful empirically: given a set of asset prices \(p\) and the second moments \(\mathbb E(xx')\) of their payoffs, (4.1) hands you a discount factor lying inside the space spanned by those assets.

Any discount factor \(m\) that prices the payoffs in \(X\) can be written \(m=x^*+\varepsilon\), with \(\mathbb E(\varepsilon x)=0\) (\(\varepsilon\) is orthogonal to every payoff). In other words, \(x^*\) is the orthogonal projection of \(m\) onto the payoff space, \(x^*=\operatorname{proj}(m\mid X)\) — the "mimicking portfolio" for the discount factor. Pricing uses only the part of \(m\) that lies in the payoff space; the orthogonal piece \(\varepsilon\) contributes nothing to pricing any tradeable payoff. This echoes the Ch 1 lesson that idiosyncratic risk is not priced.

存在性这一结论可追溯到 Ross (1978) 与 Rubinstein (1976);其与无套利、风险中性定价的联系由 Harrison and Kreps (1979) 系统化;连续时间与无穷维的处理见 Hansen and Richard (1987)。

The existence result traces to Ross (1978) and Rubinstein (1976); its connection to no-arbitrage and risk-neutral pricing was systematized by Harrison and Kreps (1979); the continuous-time and infinite-dimensional treatment is in Hansen and Richard (1987).

4.2 无套利与正的贴现因子 / No-Arbitrage and Positive Discount Factors

一价定律只给出存在一个贴现因子 \(x^*\),它未必为正——\(x^*\) 在某些状态可以取负值。要得到严格为正的贴现因子,需要一个更强(但仍很经济直觉)的条件:无套利。

4.2 No-Arbitrage and Positive Discount Factors

The law of one price gives only the existence of a discount factor \(x^*\), which need not be positive — \(x^*\) can take negative values in some states. To obtain a strictly positive discount factor we need a stronger (but still very intuitive) condition: no-arbitrage.

无套利的定义 / Definition of absence of arbitrage 不存在套利:若一个支付几乎处处非负(\(x\ge 0\) a.s.)且以正概率严格为正(\(x>0\) with positive probability),则其价格必为正,\(p(x)>0\)。直观:一个永不亏、有时赚的"东西"不可能免费或负价拿到。Absence of arbitrage: if a payoff is non-negative almost surely (\(x\ge 0\) a.s.) and strictly positive with positive probability (\(x>0\) with positive probability), then its price must be positive, \(p(x)>0\). Intuition: something that never loses and sometimes pays cannot be had for free or for a negative price.

一个方向(易):\(m>0\Rightarrow\) 无套利。 若存在 \(m>0\) 使 \(p=\mathbb E(mx)\),则对任何 \(x\ge0\)、且以正概率 \(x>0\) 的支付,\(p(x)=\mathbb E(mx)>0\)(正数乘非负、且有正概率严格为正的乘积,期望为正)。故正贴现因子的存在排除了套利。

另一个方向(难,更有用):无套利 + 一价定律 \(\Rightarrow\) 存在 \(m>0\)。 这正是资产定价的核心存在性定理。证明用分离超平面定理:把支付与其(负)价格打包成 \(\mathbb R^{S+1}\) 中的集合

One direction (easy): \(m>0\Rightarrow\) no-arbitrage. If some \(m>0\) satisfies \(p=\mathbb E(mx)\), then for any payoff with \(x\ge0\) and \(x>0\) with positive probability, \(p(x)=\mathbb E(mx)>0\) (the expectation of a positive number times a non-negative payoff that is strictly positive with positive probability). So the existence of a positive discount factor rules out arbitrage.

The other direction (hard, and more useful): no-arbitrage + law of one price \(\Rightarrow\) a positive \(m\) exists. This is the central existence theorem of asset pricing. The proof uses the separating hyperplane theorem: bundle each payoff with its (negative) price into a set in \(\mathbb R^{S+1}\),

$$M=\bigl\{(-p(x),\,x):x\in X\bigr\}\subset\mathbb R^{S+1}.$$

无套利意味着 \(M\) 与正卦限 \(\mathbb R^{S+1}_+\) 只在原点相交。两个不相交的凸集可被一张超平面分离,其法向量 \((1,m)\)(适当归一)的各分量严格为正,这就给出 \(m>0\) 且 \(p(x)=\mathbb E(mx)\)。

No-arbitrage means \(M\) intersects the positive orthant \(\mathbb R^{S+1}_+\) only at the origin. Two disjoint convex sets can be separated by a hyperplane, whose normal vector \((1,m)\) (suitably normalized) has strictly positive components — and that delivers \(m>0\) with \(p(x)=\mathbb E(mx)\).

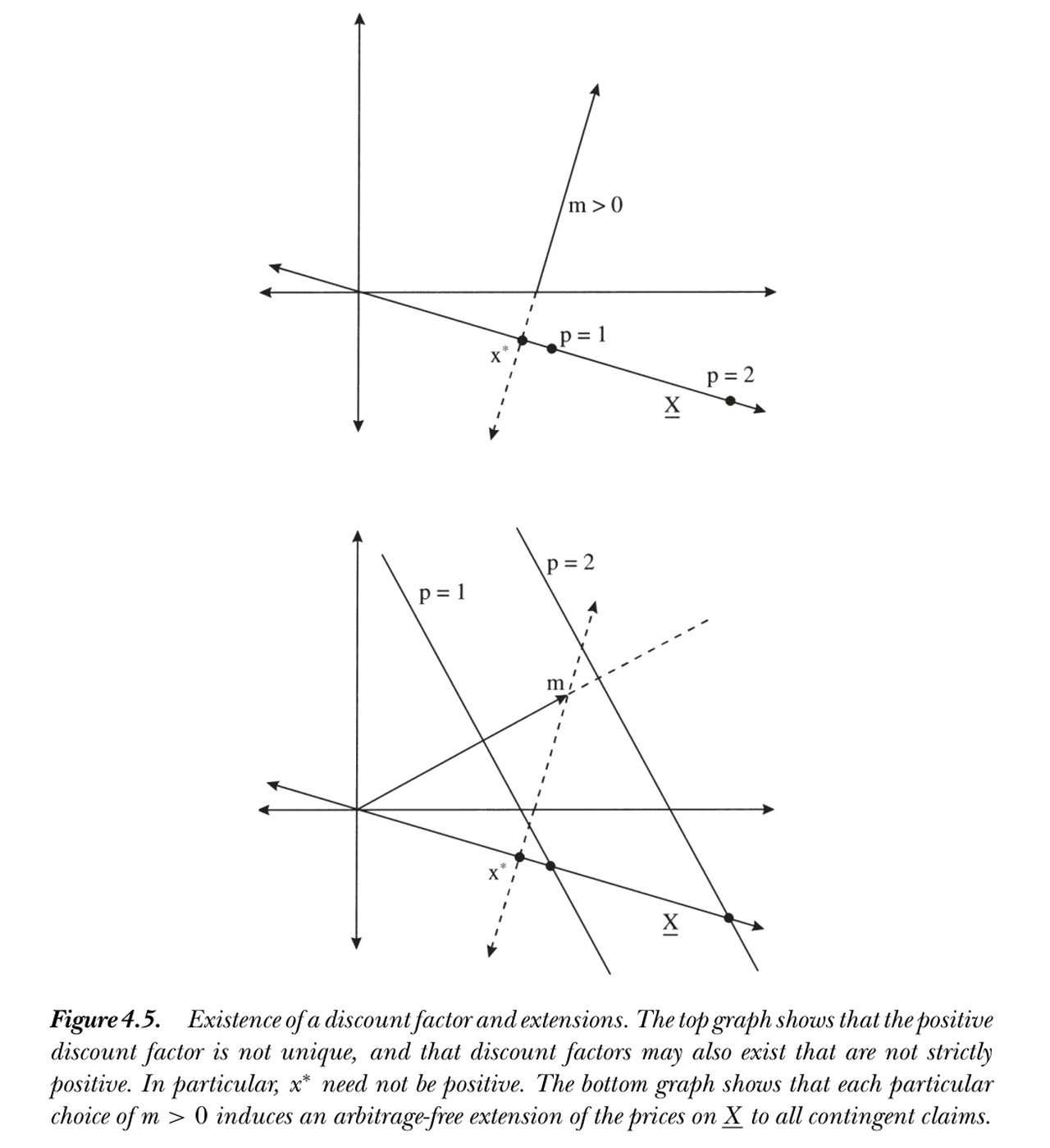

不唯一,且每个 \(m>0\) 都是一种"无套利扩张" / Not unique — each \(m>0\) is an arbitrage-free extension 这样的正贴现因子不唯一:在不完全市场里,分离超平面有许多条,每条对应一个不同的 \(m>0\)。每一个 \(m>0\) 都把定价函数从可交易支付 \(X\) 扩张到全部或有索取权 \(\mathbb R^S\),且这种扩张不引入套利。完全市场下扩张唯一(\(m=x^*\));不完全市场下,选哪个 \(m\) 就是在选如何给不可交易支付定价。Such a positive discount factor is not unique: in an incomplete market there are many separating hyperplanes, each giving a different \(m>0\). Each \(m>0\) extends the pricing function from tradeable payoffs \(X\) to all contingent claims \(\mathbb R^S\) without introducing arbitrage. In a complete market the extension is unique (\(m=x^*\)); in an incomplete market, choosing an \(m\) is choosing how to price the non-tradeable payoffs.

下图(图 4.5)画出了不唯一与扩张。上图:正贴现因子 \(m>0\) 不唯一,且支付空间内的 \(x^*\) 未必为正;下图:每选定一个 \(m>0\),就把 \(\underline X\) 上的价格无套利地扩张到所有或有索取权。

图 4.5 贴现因子的存在与扩张。上图:正贴现因子不唯一,且也存在不严格为正的贴现因子——\(x^*\) 未必为正。下图:每一个 \(m>0\) 都把 \(\underline X\) 上的价格无套利地扩张到所有或有索取权。

Figure 4.5 Existence of a discount factor and extensions. Top: the positive discount factor is not unique, and discount factors that are not strictly positive exist too — \(x^*\) need not be positive. Bottom: each choice of \(m>0\) induces an arbitrage-free extension of the prices on \(\underline X\) to all contingent claims.

4.3 另一种表达式与连续时间 / An Alternative Formula and Continuous Time

公式 (4.1) 用二阶矩 \(\mathbb E(xx')\) 表示 \(x^*\)。换用均值与协方差 \(\Sigma=\operatorname{cov}(x)\) 表示常更直观。令 \(\mathbb E(x^*)\) 待定,可证

4.3 An Alternative Formula and Continuous Time

Formula (4.1) expresses \(x^*\) via the second moment \(\mathbb E(xx')\). It is often more intuitive to use means and the covariance matrix \(\Sigma=\operatorname{cov}(x)\) instead. With \(\mathbb E(x^*)\) to be determined, one can show

$$x^*=\mathbb E(x^*)+\bigl[p-\mathbb E(x^*)\,\mathbb E(x)\bigr]'\,\Sigma^{-1}\bigl(x-\mathbb E(x)\bigr),\qquad \Sigma=\operatorname{cov}(x).\tag{4.2}$$

(4.2) 把 \(x^*\) 写成"常数 + 对去均值支付的回归"形式:贴现因子是支付的线性函数,回归系数由价格与协方差结构决定。对超额收益 \(R^e\)(价格为零)这一式简化为 Hansen and Jagannathan (1991) 用来构造贴现因子边界的形式——这是第 5 章 Hansen-Jagannathan 界的起点。

把这一构造推广到连续时间。设资产价格服从扩散过程,瞬时超额收益的漂移与扩散为 \(\mu\) 与 \(\sigma\),则贴现因子过程 \(\Lambda\) 满足

(4.2) writes \(x^*\) as "a constant plus a regression on demeaned payoffs": the discount factor is a linear function of the payoffs, with regression coefficients set by the prices and the covariance structure. For excess returns \(R^e\) (zero price) this reduces to the form Hansen and Jagannathan (1991) use to build discount-factor bounds — the starting point for the Hansen-Jagannathan bounds of Ch 5.

This construction extends to continuous time. With asset prices following diffusions whose instantaneous excess returns have drift \(\mu\) and diffusion \(\sigma\), the discount-factor process \(\Lambda\) satisfies

$$\frac{d\Lambda}{\Lambda}=-r^f\,dt-\bigl(\mu+D/p-r^f\bigr)'\,\Sigma^{-1}\sigma\,dz,\qquad \Sigma=\sigma\sigma'.\tag{4.3}$$

(4.3) 是 (4.2) 的连续时间对应:贴现因子的漂移给出无风险利率 \(-r^f\),其扩散载荷由资产的瞬时超额收益(含红利率 \(D/p\))经协方差 \(\Sigma=\sigma\sigma'\) 调整后决定。\(x^*\)(以及 \(\Lambda\))始终是落在可交易资产张成空间内的那个贴现因子。

(4.3) is the continuous-time counterpart of (4.2): the drift of the discount factor gives minus the risk-free rate \(-r^f\), and its diffusion loadings are set by the assets' instantaneous excess returns (including the dividend yield \(D/p\)), adjusted through the covariance \(\Sigma=\sigma\sigma'\). As before, \(x^*\) (and \(\Lambda\)) is the discount factor lying inside the span of the tradeable assets.

小结 / Summary

本章的逻辑链非常干净:一价定律 \(\Rightarrow\) 存在贴现因子 \(x^*\)(公式 (4.1),但未必为正);无套利 \(\Rightarrow\) 存在正贴现因子 \(m>0\)(分离超平面,但不唯一)。\(x^*=\operatorname{proj}(m\mid X)\) 是 \(m\) 在支付空间上的投影。完全市场下 \(m=x^*\) 唯一;不完全市场下,\(m>0\) 的多样性恰对应给不可交易支付定价的自由度。这为后续 Hansen-Jagannathan 界、贝塔表示与因子模型铺平了道路。

Summary

The logic of this chapter is very clean: law of one price \(\Rightarrow\) a discount factor \(x^*\) exists (formula (4.1), but not necessarily positive); no-arbitrage \(\Rightarrow\) a positive discount factor \(m>0\) exists (separating hyperplane, but not unique). \(x^*=\operatorname{proj}(m\mid X)\) is the projection of \(m\) onto the payoff space. In a complete market \(m=x^*\) is unique; in an incomplete market, the multiplicity of \(m>0\) is exactly the freedom in how to price non-tradeable payoffs. This paves the way for the Hansen-Jagannathan bounds, beta representations, and factor models to come.

习题 / Problems

- 构造 \(x^*\)。 在两状态、两资产的例子中,由价格与支付用 (4.1) 显式算出 \(x^*\),并验证它给两资产定出正确价格。

- \(x^*\) 可正可负。 举一个无套利但 \(x^*\) 在某状态为负的例子,说明为何这不构成套利(提示:\(x^*\) 本身未必是可交易支付里"非负且正概率为正"的那种)。

- 扩张的不唯一性。 在一个不完全市场里,画出两条不同的分离超平面,对应两个不同的 \(m>0\),并说明它们给同一个可交易支付定出相同价格、却给某个不可交易支付定出不同价格。

Problems

- Construct \(x^*\). In a two-state, two-asset example, compute \(x^*\) explicitly from prices and payoffs using (4.1), and verify it prices both assets correctly.

- \(x^*\) can be negative. Give an example with no arbitrage in which \(x^*\) is negative in some state, and explain why this is not an arbitrage (hint: \(x^*\) itself need not be one of the "non-negative, positive with positive probability" tradeable payoffs).

- Non-uniqueness of the extension. In an incomplete market, draw two different separating hyperplanes corresponding to two different \(m>0\), and show they assign the same price to a given tradeable payoff but different prices to some non-tradeable payoff.